In real terms, the amount of debt accumulated by households has increased at the same rate as inflation.

South Africans are a lot poorer than they were five years ago due to high debt and low income, with the result that many are struggling to acquire assets such as cars and property.

According to the Momentum/Unisa Household Net Wealth Index, South African households’ real net wealth declined by R237 billion in the third quarter of 2019, compared with the second quarter and was R133.7 billion less than in the third quarter of 2018.

The real value of household assets decreased by R240.9 billion between Q2 and Q3, to R8 381.9 billion – despite households increasing their savings to pension funds and retirement annuities.Read: Too many South Africans are slaves to debt

Household net wealth

Consumer assets consist of the combined values of their savings in pension and retirement instruments, financial investments and residential properties. The report states that the decline in the real value of household net wealth was almost solely caused by a decrease in the real value of households’ assets.

This is despite consumers saving more money in pension funds, which under normal circumstances should have contributed to an increase in the real value of their assets.

When expressed as a percentage of gross household income, the ratio of household net wealth declined from 276% in Q2 2019 to 266.7% in Q3 2019, as depicted in the following chart (assets, liabilities and wealth are expressed at a percentage of household gross income).

Household balance sheet variables expressed as a percentage of gross income

Source: Momentum/Unisa Household Net Wealth Index

As the real value of households’ outstanding liabilities increased less than their gross income, the ratio of their liabilities to gross income declined slightly from 54.4% in Q2 2019 to 54.2% in Q3 2019.

Johann van Tonder, researcher and economist in Momentum’s consumer insights division, says this is because a lot of households are using their salaries mostly to pay off debt, leaving very little money to acquire wealth or even save.

“What this means is that the bulk of households in SA will not have enough saved by the time they have to retire. So this puts an additional … burden on the government because there will be more people in need of grants.”

Van Tonder says this means South Africa is faced with a double problem, with “the value of assets not growing and the economy also not increasing”.

Outstanding debt

The real value of households’ outstanding liabilities decreased by R3.9 billion to R1 415.2 billion in Q3 2019 (from Q2 2019). The report states that this was R20.6 billion higher than the year before.

Consumer liabilities include outstanding credit such as housing, vehicle- and personal loans as well as credit card debt and outstanding municipal accounts.

The latter decreased, with National Treasury reporting that households’ outstanding municipal debt amounted to R111.3 billion in Q3 2019 (Q2: R115 billion). This was however mostly due to municipalities writing off debt considered not recoverable.Read: Drowning in debt and much more to come

Signs of behavioural change …

It seems consumers are at least aware of the problem and have made an effort to stop using money they don’t have:

- The rate at which households incurred credit card debt halved to 1.2% in Q3 from 2.4% in Q2; and

- Outstanding overdrafts declined by 1.6% in Q3 following a decline of 4.7% in Q2 2019.

Real outstanding mortgages increased at the slower pace of 0.3% in Q3 (0.6% in Q2), while outstanding installment sales credit decreased by 0.3% (following a decline of 0.2% in Q2).

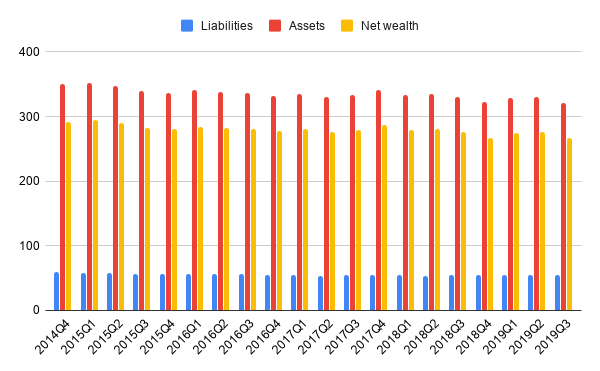

Balance sheet estimates

However in real terms, the amount of debt accumulated by households has increased at the same rate as inflation in the past five years.

In 2014 (Q4) the liabilities index was at 108.1% – and in 2019 (Q3) it was still at 108.1%, according to the Momentum/Unisa Household Net Wealth Index.

“Our assets are less than … they were in 2014,” says Van Tonder, adding that we’re a lot poorer than we were five years ago.

Trade wars and power outages

Van Tonder says international events such as the trade war between the US and China increased fears of an economic recession and further explains why household wealth declined in the third quarter of 2019 – because most of their financial assets are invested at the JSE.

Other factors contributing to the loss of household wealth include domestic issues such as Eskom and the precarious electricity supply situation, issues around state capture, and the weak local economy.

Reference: www.moneyweb.co.za/news/economy/south-africans-became-r237bn-poorer-in-2019